Growth Vs Value Stocks For Retirement Portfolios: Which Strategy Delivers Safer Income

For decades, the goal was simple. Accumulate. Buy shares, let them compound, tune out the noise. But the day you stop earning a paycheck and start drawing one from your portfolio, the question flips. It’s no longer just about how fast your investments grow. It’s about how reliably they pay you, and whether they can keep paying through a market that has no idea when you retired.

That’s the moment the debate over growth vs value stocks stops being academic. One approach hands you cash while you wait. The other asks you to sell into whatever price the market happens to offer on the day you need money. For someone living off a portfolio, that gap is the entire ballgame. Here’s how the two behave once income, not accumulation, becomes the job.

What Actually Separates Growth From Value

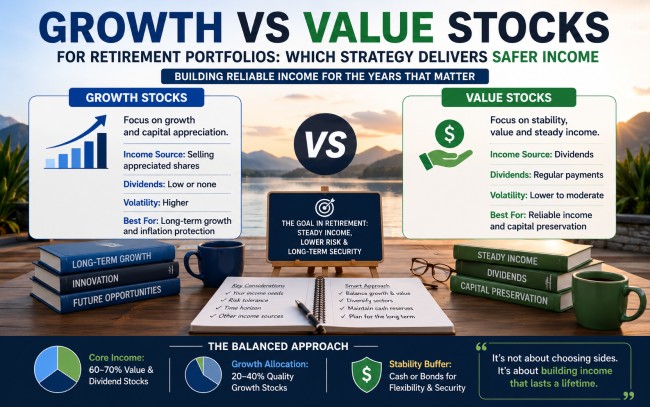

Start with the plumbing. Growth companies reinvest their earnings. Profits go back into expansion, hiring, product, market share, and they usually pay little or no dividend. You make money when the price climbs, full stop. Picture the fast-scaling names that ran the last decade: rich valuations, big expectations, returns riding almost entirely on the stock going up.

Value companies run on a different engine. They tend to be mature, cash-generating businesses priced below what their fundamentals suggest they’re worth. Lower price-to-earnings and price-to-book ratios, and often, a habit of paying shareholders in cash through dividends. Utilities, established consumer staples, banks, pipelines. Unexciting. That’s rather the point.

Before you tilt a portfolio toward either camp, it pays to see the full picture. A deeper breakdown of growth vs value stocks and the valuation mechanics underneath them lays out more than most retirees are ever shown.

Where Retirement Income Actually Comes From

Most accumulation-era advice glosses over something simple. A stock puts money in your pocket exactly two ways. It pays you a dividend, or you sell a piece of it. Growth investing leans almost entirely on the second. Value and dividend investing lean on the first.

That distinction outweighs any single year’s return number, because of a risk that barely exists while you’re working: sequence-of-returns risk. If a downturn lands early in retirement and you’re forced to sell shares to cover living costs, you lock in the loss and permanently shrink the base that’s supposed to recover later. Selling growth shares into a bear market to pay the bills is how portfolios that “should have lasted” quietly run dry.

Dividends step around that trap. A company paying you cash every quarter doesn’t ask you to sell anything at a bad price. The income shows up whether the ticker is green or red.

Comparing The Two On What Matters After You Retire

| Factor | Growth Stocks | Value Stocks |

| Main income source | Selling appreciated shares | Dividends |

| Typical volatility | Higher | Lower to moderate |

| Behavior in downturns | Often falls hardest | Tends to hold up better |

| Sensitivity to rising rates | More vulnerable | More resilient |

| Cash flow to the retiree | Irregular, self-funded | Regular, company-funded |

None of this makes growth the villain. It makes growth a different tool. Over long stretches, the growth vs value stocks contest has swung both ways. Growth ran away with the 2010s in a low-rate world. Value clawed back relevance once rates rose and investors started caring about cash flow they could see today. Decades of academic research also point to a long-run value premium, though it arrives unevenly and can vanish for years at a stretch.

For a 40-year-old, riding out those swings is no problem. For a 68-year-old pulling income, the swings are the problem.

Why Going All-In On Either Side Usually Backfires

Purists on both sides of the growth vs value stocks debate tend to oversell their own team.

An all-value, all-dividend portfolio feels safe right up until you notice you’ve concentrated into a few mature sectors, accepted slower total growth, and tied yourself to companies that can cut dividends exactly when the economy sours. A dividend is a policy, not a promise.

An all-growth portfolio in retirement is arguably worse. You’ve built an income machine that generates no income, so you fund withdrawals by selling shares, in the most volatile corner of the market, on the market’s schedule rather than yours. Wonderful in a rising market. Brutal in a falling one.

Most durable retirement income plans settle somewhere in between, and the balance usually tilts toward value:

- A core of quality dividend payers to cover the bulk of predictable expenses

- A measured slice of growth for long-term appreciation and a hedge against inflation

- Enough cash or short-term bonds that you’re never forced to sell stocks at the wrong moment

Your right mix depends on what you spend, what else pays you (Social Security, a pension), and how well you sleep when balances drop.

Conclusion

If safer means steadier cash that doesn’t hinge on selling into a slump, value and dividend-focused stocks win on structure alone. They were built to pay you.

But safe income and a safe portfolio aren’t the same thing. Lean entirely on income stocks and you invite a slower failure: inflation grinding down your purchasing power across a retirement that could run 30 years. The retiree who held only “safe” payers at 65 can watch those fixed dividends buy noticeably less at 85.

So the growth vs value stocks question isn’t really a contest between two rival camps. It’s a question of proportion, set against your timeline and your need for cash now versus cash decades out.

Weight income-producing quality toward the money you’ll spend soon. Let a measured piece of growth defend the money you won’t touch for years. That, more than any label, is how thoughtful retirees answer the growth vs value stocks question and actually live off the result.